From the PM Desk - Staying Invested Without Standing Still

Welcome to From the PM Desk, a new regular series where our portfolio management team connects market headlines to real portfolio decisions. Written for advisors, this commentary is part of our commitment to transparency and to sharing how we think, assess risk, and position portfolios through changing markets.

Key Takeaways

- The conflict between the U.S. and Iran introduces a source of potentially prolonged market uncertainty. While markets have remained resilient as of this writing (May 14, 2026), history suggests conflicts may unfold over months, not weeks.

- When outcomes widen, maintaining diversification is critical. Maintaining exposure across regions, sectors, and individual securities remains one of our most powerful risk-mitigating tools in this environment.

- We have actively positioned our portfolios to deliver resiliency through a wide range of outcomes. We trimmed equity overweights and rebalanced the fixed income positioning in our portfolios to emphasize diversification, improve overall credit quality, and reduce reliance on spread‑driven sources of return.

The conflict between the United States and Iran has introduced a new and persistent source of uncertainty for global markets. While financial markets have so far taken the developments in stride, we believe it is now reasonable to expect the resolution to unfold over months—not weeks. A longer-duration conflict will likely have wide-ranging second- and third-order effects that are impossible to forecast precisely but important to manage thoughtfully.

A Longer-Duration Conflict Is the Central Risk

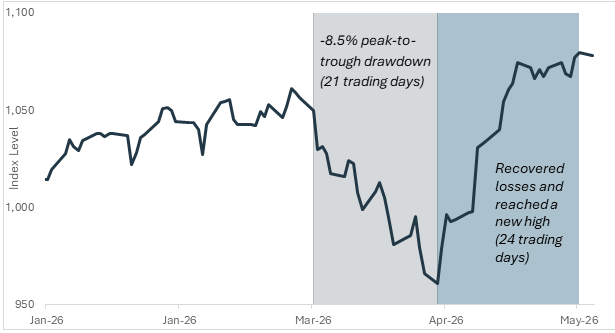

Early market reactions often underestimate how long conflicts last. Exhibit 1 shows the MSCI All Country World Index since the beginning of the year, with the shaded area representing the days since the Iran conflict began.

We see that equity markets quickly responded to the conflict, with concerns over growth and inflation incorporated into investors’ expectations. And yet investors just as quickly looked through the conflict, potentially believing resolution was in the near term. The index drew down 8.5% and then recovered to hit new all-time highs in just 45 trading days.

Exhibit 1—Year to Date Performance of Global Equities

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. Note: views are from a U.S. dollar perspective. This material is an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Global Equities as represented by the MSCI All Country World Index. Source: MSCI and FactSet. Data as of May 5, 2026.

It is certainly possible that the conflict ends in short order, and we hope it does. Many headlines, as of this writing, are discussing the increasing probability of a ceasefire. But we believe it will not be “over” until the Strait of Hormuz is open—the strategic and economic importance of the closure will remain a major overhang on the global economy until oil flows freely through the strait. Even if the conflict ended permanently today, it would take months to return to a position of free trade through the strait.

For example, the Pentagon briefed Congress that it may take six months to fully demine the Strait of Hormuz. And this assumption ignores all the damage to energy infrastructure that has occurred in the region. In optimistic scenarios, clearing shipping lanes, repairing damaged infrastructure, and restoring confidence among insurers and shipping companies takes time measured in months if not years.

With a substantial share of global oil and refined products temporarily removed from circulation, the remaining options are inventory drawdowns (countries releasing strategic reserves, oil in storage at terminals or on ships in transit) and curtailing demand—neither of which can persist indefinitely. Ramping up production from countries like the U.S., to fill this gap, would still take months.

In short, markets may be pricing a shorter disruption than the underlying physical realities suggest.

This mismatch between market pricing and plausible timelines creates a wide range of outcomes for asset prices, inflation, and growth. Precisely the type of environment where diversification matters most.

Why Broad Diversification Matters More Than Ever

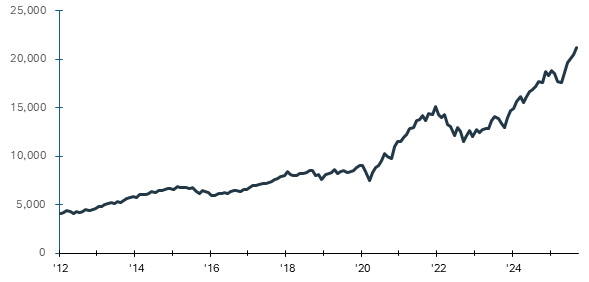

Broad diversification is the most effective tool we have for managing uncertainty of this kind. While the United States is now a net exporter of energy, the global financial system is still deeply interconnected. Many U.S. assets are owned by foreign investors, and many of those investors live in regions that are highly dependent on energy imports from the Middle East.

Data from the Federal Reserve shows the scale of foreign ownership of U.S. assets. Exhibit 2 shows the share of U.S. corporate stock held by non-U.S. investors. As of the latest available data, non-U.S. investors hold over $21 trillion in U.S. corporate stock. This represents about 36% of the U.S. equity market, as measured by the S&P 1500 Index. Consider that the demand for oil (and its derivative products such as fertilizers and diesel) is largely inelastic. If foreign investors need to liquidate assets to fund essential energy imports, U.S. equities could face selling pressure unrelated to domestic fundamentals.

Exhibit 2—Foreign Ownership in U.S. Stocks Continues to Increase (in billions)

Past performance is not a reliable indicator of current or future results. This material is an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management, FRED, Bureau of Economic Analysis. Data from January 2012 through September 2025

When energy prices rise sharply, countries with limited domestic supply often face a difficult tradeoff: draw down reserves, accept slower growth, or liquidate foreign assets to fund essential imports. That dynamic is exactly the type of second-order effect that may impact portfolios for a longer duration.

Rather than trying to forecast which markets or sectors will feel these effects most acutely, we believe portfolios are best positioned by maintaining exposure across companies, sectors, and regions. Diversification does not eliminate risk, but it reduces reliance on any single outcome being “right.”

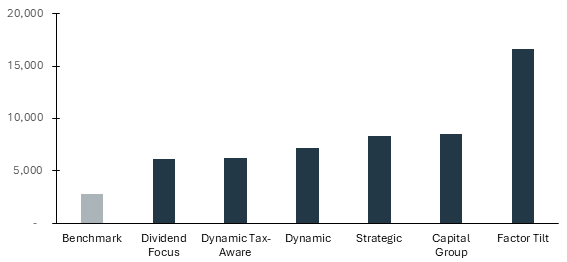

One way to measure diversification is the number of securities a portfolio owns. The KIM portfolios are all more broadly diversified than their benchmark by this measure, and meaningfully so.

Exhibit 3 — Number of Individual Securities in KIM Portfolios and Benchmark

Past performance is not a reliable indicator of current or future results. This material is an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management, FactSet. Data as of May 5, 2026 or the latest reported date for the underlying investment. Number of individual securities represents the unique securities held in the Equity risk profile for each model series. The Benchmark consists of a blend of the MSCI All Country World Index and the MSCI USA Index.

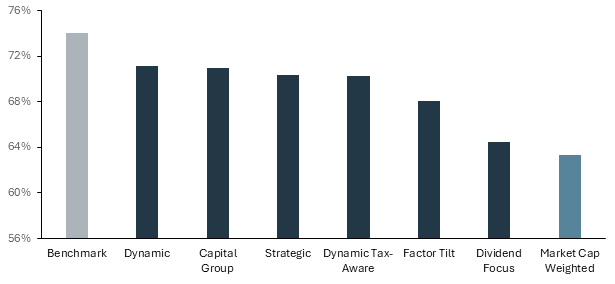

Beyond the number of holdings, KIM portfolios are also broadly diversified across countries. While all portfolios maintain a deliberate U.S. home bias—consistent with the construction of our benchmark—the magnitude of that exposure is intentional. Our benchmark allocates roughly 74% to U.S. equities, compared with about 63% in a market cap weighted global equity portfolio.

As shown in Exhibit 4, this means we are structurally underweight U.S. equities relative to our benchmark, while still maintaining a home bias relative to the global market. Given the U.S. market’s concentration (where performance is increasingly driven by a small group of large companies with similar growth drivers) this positioning reflects our commitment to broad diversification without abandoning the benefits of home‑market exposure.

Exhibit 4 — U.S Equity Weight in KIM Portfolios and Benchmark

Past performance is not a reliable indicator of current or future results. This material is an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management, FactSet. Data as of May 5, 2026 or the latest reported date for the underlying investment. U.S equity weight represents the holdings held in the Equity risk profile for each model series. The Benchmark consists of 68.6% MSCI All Country World Index and 29.4% MSCI USA Index. Market Neutral is represented by the MSCI All Country World Index.

The U.S. Economy: Resilient, Not Immune

Importantly, none of this uncertainty suggests that the U.S. economy is on the brink of recession. It’s certainly survived and thrived through other periods of change and uncertainty. We see the U.S. economy remaining driven by productivity and policy.

That said, resilience is not the same as immunity. Rising energy prices are beginning to flow into the economy, and consumer spending has softened at the margin. Offsetting forces—including tax refunds, a positive wealth effect from equity markets, and increased defense spending—are helping cushion the impact, but risks appear skewed toward the second half of the year.

At the start of the year, KIM portfolios were positioned with a modest equity overweight of roughly 2–4% relative to their strategic risk profiles. For example, the KIM Dynamic 60/40 portfolio held closer to 64% in equities.

As the year has progressed, we have weighed continued earnings strength and a robust capital‑expenditure pipeline—supportive of productivity and growth—against rising global conflict and policy uncertainty. In response, we intentionally moderated risk across portfolios, reducing the equity overweight to approximately 1–2%. This positioning recognizes the risks of a sustained conflict, while remaining mindful that markets have historically compensated investors for geopolitical risk.

Fixed Income Positioning in a Prolonged Conflict

A sustained geopolitical conflict tied to energy markets also complicates the outlook for interest rates. Higher energy prices act like a tax on consumers and businesses, raising headline inflation even if underlying inflation pressures remain contained. At the same time, elevated deficits (which seem increasingly difficult to untangle), increased defense spending, and the possibility of foreign selling of U.S. debt may introduce upward pressure on Treasury yields.

With credit spreads near historically tight levels, we adjusted the fixed income positioning in our portfolios to emphasize diversification, improve overall credit quality, and reduce reliance on spread‑driven sources of return.

Most KIM model portfolios are positioned with shorter duration than their respective benchmarks, reflecting an interest rate risk environment that offers little margin for error. The primary exceptions are the Factor Tilt portfolio (where consistent exposure to term and credit premiums is by design) and our Tax‑Aware portfolios, where the municipal bond curve presents a different risk-reward tradeoff than the taxable bond market.

Positioning for Uncertainty

Geopolitically driven disruptions to energy markets create a difficult backdrop because timelines stretch and outcomes become increasingly difficult to predict. In this case, the constraint is not just uncertainty but rather it is the physical reality of restoring energy flows, which takes time. That keeps a wide range of outcomes on the table for growth, inflation, and asset prices.

Our response has been straightforward: reduce reliance on any single outcome and position portfolios to absorb volatility without sacrificing long-term return potential.

Across portfolios, we have:

- Moderated equity risk by trimming overweights

- Maintained broad exposure across regions and sectors

- Emphasized higher-quality fixed income with shorter duration

- Reduced dependence on credit spreads as a primary source of return

Each of these decisions reflects our objective of building portfolios that can navigate a prolonged period of uncertainty rather than react to each headline.

Markets will continue to adjust as information emerges. Our focus remains on disciplined positioning—staying invested, managing risk deliberately, and ensuring portfolios are built to withstand a range of scenarios, not just the one that proves correct.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.